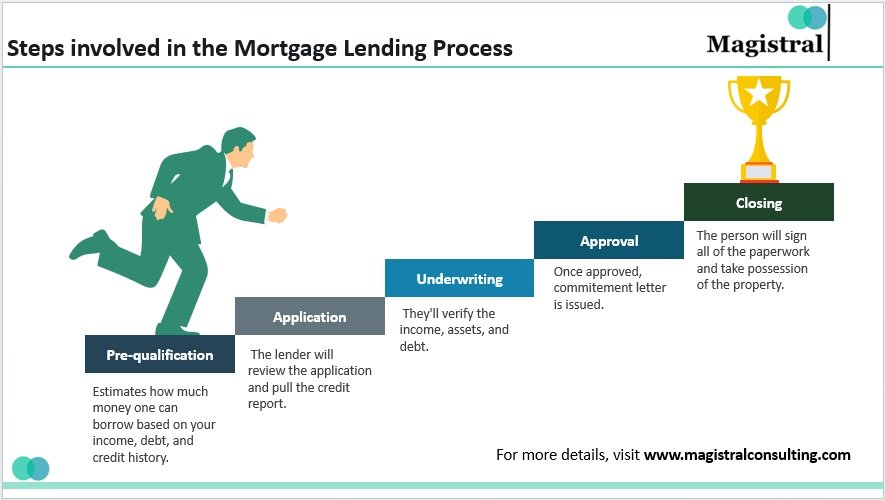

Buying a home is a life-changing experience, but understanding the financial mechanics behind it can feel complex. A mortgage is more than just a monthly payment—it’s a structured loan designed to help you own your home while spreading out costs over time. In this article, we’ll break down how does a mortgage work in simple terms, using practical examples, tables, and FAQs to give you a clear understanding of this essential financial tool.

What Is a Mortgage?

A mortgage is a loan from a bank or lender that allows you to purchase a property without paying the full price upfront. In exchange, you agree to pay back the loan over a set period, usually 15 to 30 years, with interest.

The loan typically includes:

- Principal: The amount you borrowed.

- Interest: The cost of borrowing the principal.

- Taxes and Insurance: Many lenders include property taxes and homeowners insurance in monthly payments.

Understanding these components is the first step to knowing how does a mortgage work in practice.

1. How Monthly Mortgage Payments Are Calculated

Your monthly mortgage payment depends on three key elements: principal, interest, and term length. Early in the loan, a larger portion of your payment goes toward interest, while later, more goes toward principal.

Example Table: Mortgage Payment Breakdown

| Loan Amount | Interest Rate | Term (Years) | Monthly Payment | Principal vs Interest (Year 1) |

|---|---|---|---|---|

| $300,000 | 6% | 30 | $1,798 | $450 / $1,348 |

| $400,000 | 5.5% | 20 | $2,790 | $1,250 / $1,540 |

| $500,000 | 6.5% | 30 | $3,160 | $700 / $2,460 |

This table illustrates how monthly payments vary based on interest rates, loan amounts, and terms, helping you understand how does a mortgage work on a practical level.

2. Fixed-Rate vs Adjustable-Rate Mortgages

Mortgages generally fall into two main categories:

- Fixed-Rate Mortgage (FRM): The interest rate stays the same throughout the loan. This provides predictable payments and makes long-term budgeting easier.

- Adjustable-Rate Mortgage (ARM): The interest rate changes periodically, usually after an initial fixed period. Payments may increase or decrease, affecting how your mortgage works over time.

Comparison Table: Fixed vs Adjustable

| Feature | Fixed-Rate Mortgage | Adjustable-Rate Mortgage |

|---|---|---|

| Interest Rate | Fixed | Variable |

| Monthly Payment | Predictable | Can fluctuate |

| Best For | Long-term stability | Short-term savings or flexibility |

| Example Loan | 30-year FRM | 5/1 ARM |

Understanding these differences is crucial to know how does a mortgage work for your unique financial situation.

3. Understanding Amortization

Amortization is the process of gradually paying off your mortgage through regular payments. Each payment covers both interest and principal, reducing the total loan balance over time.

Amortization Table Example (First 5 Years on $300,000 at 6%)

| Year | Principal Paid | Interest Paid | Remaining Balance |

|---|---|---|---|

| 1 | $5,400 | $16,200 | $294,600 |

| 2 | $5,700 | $15,900 | $288,900 |

| 3 | $6,000 | $15,600 | $282,900 |

| 4 | $6,400 | $15,200 | $276,500 |

| 5 | $6,800 | $14,800 | $269,700 |

This shows how early payments mostly cover interest, but over time, your principal repayment increases. This structure explains much of how does a mortgage work behind the scenes.

4. Additional Costs in a Mortgage

A mortgage doesn’t only include principal and interest. Other components affect your total payment:

- Property Taxes: Often collected monthly via escrow.

- Homeowners Insurance: Protects your home against damage or theft.

- Private Mortgage Insurance (PMI): Required if your down payment is less than 20%.

- HOA Fees: Applicable if you live in a community with a homeowners association.

Mortgage Cost Table Example

| Component | Estimated Monthly Cost | Notes |

|---|---|---|

| Principal & Interest | $1,798 | Based on $300,000 loan |

| Property Taxes | $300 | Varies by location |

| Homeowners Insurance | $100 | Required by lender |

| PMI | $150 | If down payment <20% |

| Total Monthly Payment | $2,348 | Full estimated cost |

This table helps homeowners understand the real costs involved and clarifies how does a mortgage work financially each month.

5. Down Payments and Their Impact

Your down payment affects your mortgage in two ways:

- Reduces the loan principal.

- May reduce or eliminate PMI if you pay 20% or more upfront.

Example Table: Down Payment Impact

| Home Price | Down Payment | Loan Amount | Monthly Payment (30yr, 6%) | PMI Needed |

|---|---|---|---|---|

| $300,000 | $15,000 (5%) | $285,000 | $1,709 | Yes |

| $300,000 | $60,000 (20%) | $240,000 | $1,439 | No |

| $300,000 | $30,000 (10%) | $270,000 | $1,619 | Yes |

This illustrates how down payments influence how your mortgage works over time, showing that even small changes can affect your financial outcome.

6. Prepayment Options

Many borrowers want to know how does a mortgage work if they make extra payments. Prepayment is paying more than your scheduled monthly amount. Benefits include:

- Reducing total interest paid.

- Shortening loan term.

- Building home equity faster.

Always check for prepayment penalties before making extra payments.

FAQs

1. How does a mortgage work if I make extra payments?

Extra payments typically reduce the principal, lowering interest and shortening your loan term.

2. Does an ARM mortgage cost more in the long run?

It depends on interest rate changes. ARMs can save money initially but may increase costs if rates rise.

3. What is PMI and how does it affect my mortgage?

Private Mortgage Insurance protects lenders when down payments are below 20%. It increases monthly payments until sufficient equity is built.

4. Can I pay off my mortgage early?

Yes, but check your mortgage agreement for prepayment penalties. Early payoff reduces interest costs.

5. How much should I put as a down payment?

While 20% eliminates PMI, smaller down payments are possible. The higher your down payment, the lower your monthly payment and total interest.